Balance of trade

The balance of trade (or net exports, sometimes symbolized as NX) is the difference between the monetary value of exports and imports of output in an economy over a certain period. It is the relationship between a nation's imports and exports.[1] A positive or favorable balance of trade is known as a trade surplus if it consists of exporting more than is imported; a negative or unfavorable balance is referred to as a trade deficit or, informally, a trade gap. The balance of trade is sometimes divided into a goods and a services balance.

Early understanding of the functioning of balance of trade informed the economic policies of Early Modern Europe that are grouped under the heading mercantilism. An early statement appeared in Discourse of the Common Weal of this Realm of England, 1549: "We must always take heed that we buy no more from strangers than we sell them, for so should we impoverish ourselves and enrich them."[2]

Definition

The balance of trade forms part of the current account, which includes other transactions such as income from the international investment position as well as international aid. If the current account is in surplus, the country's net international asset position increases correspondingly. Equally, a deficit decreases the net international asset position.

The trade balance is identical to the difference between a country's output and its domestic demand (the difference between what goods a country produces and how many goods it buys from abroad; this does not include money re-spent on foreign stock, nor does it factor in the concept of importing goods to produce for the domestic market).

Measuring the balance of trade can be problematic because of problems with recording and collecting data. As an illustration of this problem, when official data for all the world's countries are added up, exports exceed imports by a few percent; it appears the world is running a positive balance of trade with itself. This cannot be true, because all transactions involve an equal credit or debit in the account of each nation. The discrepancy is widely believed to be explained by transactions intended to launder money or evade taxes, smuggling and other visibility problems. However, especially for developed countries, accuracy is likely.

Factors that can affect the balance of trade include:

- The cost of production (land, labor, capital, taxes, incentives, etc.) in the exporting economy vis-à-vis those in the importing economy;

- The cost and availability of raw materials, intermediate goods and other inputs;

- Exchange rate movements;

- Multilateral, bilateral and unilateral taxes or restrictions on trade;

- Non-tariff barriers such as environmental, health or safety standards;

- The availability of adequate foreign exchange with which to pay for imports; and

- Prices of goods manufactured at home (influenced by the responsiveness of supply)

In addition, the trade balance is likely to differ across the business cycle. In export-led growth (such as oil and early industrial goods), the balance of trade will improve during an economic expansion. However, with domestic demand led growth (as in the United States and Australia) the trade balance will worsen at the same stage in the business cycle.

Since the mid 1980s, the United States has had a growing deficit in tradeable goods, especially with Asian nations (China and Japan) which now hold large sums of U.S debt that has funded the consumption.[3][4] The U.S. has a trade surplus with nations such as Australia. The issue of trade deficits can be complex. Trade deficits generated in tradeable goods such as manufactured goods or software may impact domestic employment to different degrees than trade deficits in raw materials.

Economies such as Canada, Japan, and Germany which have savings surpluses, typically run trade surpluses. China, a high growth economy, has tended to run trade surpluses. A higher savings rate generally corresponds to a trade surplus. Correspondingly, the U.S. with its lower savings rate has tended to run high trade deficits, especially with Asian nations.

Views on economic impact

Conditions where trade imbalances may be problematic

Those who ignore the effects of long run trade deficits may be confusing David Ricardo's principle of comparative advantage with Adam Smith's principle of absolute advantage, specifically ignoring the latter. The economist Paul Craig Roberts notes that the comparative advantage principles developed by David Ricardo do not hold where the factors of production are internationally mobile.[5][6] Global labor arbitrage, a phenomenon described by economist Stephen S. Roach, where one country exploits the cheap labor of another, would be a case of absolute advantage that is not mutually beneficial.[7][8][9]

Since the stagflation of the 1970s, the U.S. economy has been characterized by slower GDP growth. In 1985, the U.S. began its growing trade deficit with China. Over the long run, nations with trade surpluses tend also to have a savings surplus. The U.S. has been plagued by persistently lower savings rates than its trading partners which tend to have trade surpluses. Germany, France, Japan, and Canada have maintained higher savings rates than the U.S. over the long run.[10] Some economists believe that GDP and employment can be dragged down by an over-large deficit over the long run.[11][12] The opportunity cost of a forgone tax base may outweigh perceived gains, especially where artificial currency pegs and manipulations are present to distort trade.[13] Wealth-producing primary sector jobs in the U.S. such as those in manufacturing and computer software have often been replaced by much lower paying wealth-consuming jobs such those in retail and government in the service sector when the economy recovered from recessions.[6][14][15] Some economists contend that the U.S. is borrowing to fund consumption of imports while accumulating unsustainable amounts of debt.[3][16]

In 2006, the primary economic concerns centered around: high national debt ($9 trillion), high non-bank corporate debt ($9 trillion), high mortgage debt ($9 trillion), high financial institution debt ($12 trillion), high unfunded Medicare liability ($30 trillion), high unfunded Social Security liability ($12 trillion), high external debt (amount owed to foreign lenders) and a serious deterioration in the United States net international investment position (NIIP) (-24% of GDP),[3] high trade deficits, and a rise in illegal immigration.[16][17]

These issues have raised concerns among economists and unfunded liabilities were mentioned as a serious problem facing the United States in the President's 2006 State of the Union address.[17][18] On June 26 2009, Jeff Immelt, the CEO of General Electric, called for the U.S. to increase its manufacturing base employment to 20% of the workforce, commenting that the U.S. has outsourced too much in some areas and can no longer rely on the financial sector and consumer spending to drive demand.[19]

Conditions where trade imbalances may not be problematic

Small trade deficits are generally not considered to be harmful to either the importing or exporting economy. However, when a national trade imbalance expands beyond prudence (generally thought to be several percent of GDP, for several years), adjustments tend to occur. While unsustainable imbalances may persist for long periods (cf, Singapore and New Zealand’s surpluses and deficits, respectively), the distortions likely to be caused by large flows of wealth out of one economy and into another tend to become intolerable.

In simple terms, trade deficits are paid for out of foreign exchange reserves, and may continue until such reserves are depleted. At such a point, the importer can no longer continue to purchase more than is sold abroad. This is likely to have exchange rate implications: a sharp loss of value in the deficit economy’s exchange rate with the surplus economy’s currency will change the relative price of tradable goods, and facilitate a return to balance or (more likely) an over-shooting into surplus the other direction.

More complexly, an economy may be unable to export enough goods to pay for its imports, but is able to find funds elsewhere. Service exports, for example, are more than sufficient to pay for Hong Kong’s domestic goods export shortfall. In poorer countries, foreign aid may fill the gap while in rapidly developing economies a capital account surplus often off-sets a current-account deficit. Finally, there are some economies where transfers from nationals working abroad contribute significantly to paying for imports. The Philippines, Bangladesh and Mexico are examples of transfer-rich economies.

Adam Smith on trade deficits

"IN the foregoing part of this chapter I have endeavoured to show, even upon the principles of the commercial system, how unnecessary it is to lay extraordinary restraints upon the importation of goods from those countries with which the balance of trade is supposed to be disadvantageous. Nothing, however, can be more absurd than this whole doctrine of the balance of trade, upon which, not only these restraints, but almost all the other regulations of commerce are founded. When two places trade with one another, this doctrine supposes that, if the balance be even, neither of them either loses or gains; but if it leans in any degree to one side, that one of them loses and the other gains in proportion to its declension from the exact equilibrium." (Smith, 1776, book IV, ch. iii, part ii) [20]

Milton Friedman on trade deficits

In the 1980s, Milton Friedman, the Nobel Prize-winning economist and father of Monetarism, contended that some of the concerns of trade deficits are unfair criticisms in an attempt to push macroeconomic policies favorable to exporting industries.

Prof. Friedman argued that trade deficits are not necessarily important as high exports raise the value of the currency, reducing aforementioned exports, and vise versa for imports, thus naturally removing trade deficits not due to investment. Milton Friedman's son, David D. Friedman, shares this view and cites the comparative advantage concepts of David Ricardo.[21]

In the late 1970s and early 1980s, the U.S. had experienced high inflation and Friedman's policy positions tended to defend the stronger dollar at that time. He stated his belief that these trade deficits were not necessarily harmful to the economy at the time since the currency comes back to the country (country A sells to country B, country B sells to country C who buys from country A, but the trade deficit only includes A and B). However, it may be in one form or another including the possible tradeoff of foreign control of assets. In his view, the "worst case scenario" of the currency never returning to the country of origin was actually the best possible outcome: the country actually purchased its goods by exchanging them for pieces of cheaply-made paper. As Friedman put it, this would be the same result as if the exporting country burned the dollars it earned, never returning it to market circulation.[22] This position is a more refined version of the theorem first discovered by David Hume.[23] Hume argued that England could not permanently gain from exports, because hoarding gold (i.e., currency) would make gold more plentiful in England; therefore, the prices of English goods would rise, making them less attractive exports and making foreign goods more attractive imports. In this way, countries' trade balances would balance out.[24]

Friedman believed that deficits would be corrected by free markets as floating currency rates rise or fall with time to encourage or discourage imports in favor of the exports, reversing again in favor of imports as the currency gains strength. In the real world, a potential difficulty is that currency markets are far from a free market, with government and central banks being major players, and this is unlikely to change within the foreseeable future. Nevertheless, recent developments have shown that the global economy is undergoing a fundamental shift. For many years, the U.S. has borrowed and bought while in general, the rest of the world has lent and sold. However, as Friedman predicted, this paradigm appears to be changing.

As of October 2007, the U.S. dollar weakened against the euro, British pound, and many other currencies. For instance, the euro hit $1.42 in October 2007[25], the strongest it has been since its birth in 1999. Against this backdrop, American exporters are finding quite favorable overseas markets for their products and U.S. consumers are responding to their general housing slowdown by slowing their spending. Furthermore, China, the Middle East, central Europe and Africa are absorbing more of the world's imports which in the end may result in a world economy that is more evenly balanced. All of this could well add up to a major readjustment of the U.S. trade deficit, which as a percentage of GDP, began in 1991.[26]

Friedman and other economists have pointed out that a large trade deficit (importation of goods) signals that the country's currency is strong and desirable. To Friedman, a trade deficit simply meant that consumers had opportunity to purchase and enjoy more goods at lower prices; conversely, a trade surplus implied that a country was exporting goods its own citizens did not get to consume or enjoy, while paying high prices for the goods they actually received.

Friedman contended that the structure of the balance of payments was misleading. In an interview with Charlie Rose, he stated that "on the books" the US is a net borrower of funds, using those funds to pay for goods and services. He essentially claimed that the foreign assets were not carried on the books at their higher, truer value.

Friedman presented his analysis of the balance of trade in Free to Choose, widely considered his most significant popular work.

Frédéric Bastiat on the fallacy of trade deficits

The 19th century economist and philosopher Frédéric Bastiat expressed the idea that trade deficits actually were a manifestation of profit, rather than a loss. He proposed as an example to suppose that he, a Frenchman, exported French wine and imported British coal, turning a profit. He supposed he was in France, and sent a cask of wine which was worth 50 francs to England. The customhouse would record an export of 50 francs. If, in England, the wine sold for 70 francs (or the pound equivalent), which he then used to buy coal, which he imported into France, and was found to be worth 90 francs in France, he would have made a profit of 40 francs. But the customhouse would say that the value of imports exceeded that of exports and was trade deficit against the ledger of France. [27] By reductio ad absurdum, Bastiat argued that the national trade deficit was an indicator of a successful economy, rather than a failing one. Bastiat predicted that a successful, growing economy would result in greater trade deficits, and an unsuccessful, shrinking economy would result in lower trade deficits. This was later, in the 20th century, affirmed by economist Milton Friedman.

Warren Buffett on trade deficits

The successful American businessman and investor Warren Buffett was quoted in the Associated Press (January 20, 2006) as saying "The U.S trade deficit is a bigger threat to the domestic economy than either the federal budget deficit or consumer debt and could lead to political turmoil... Right now, the rest of the world owns $3 trillion more of us than we own of them." Buffett has proposed a tool called Import Certificates as a solution to the United States' problem and ensure balanced trade.[28]

John Maynard Keynes on the balance of trade

In the last few years of his life, John Maynard Keynes was much preoccupied with the question of balance in international trade. He was the leader of the British delegation to the United Nations Monetary and Financial Conference in 1944 that established the Bretton Woods system of international currency management.

He was the principal author of a proposal — the so-called Keynes Plan —— for an International Clearing Union. The two governing principles of the plan were that the problem of settling outstanding balances should be solved by 'creating' additional 'international money', and that debtor and creditor should be treated almost alike as disturbers of equilibrium. In the event, though, the plans were rejected, in part because "American opinion was naturally reluctant to accept the principal of equality of treatment so novel in debtor-creditor relationships".[29]

His view, supported by many economists and commentators at the time, was that creditor nations may be just as responsible as debtor nations for disequilibrium in exchanges and that both should be under an obligation to bring trade back into a state of balance. Failure for them to do so could have serious consequences. In the words of Geoffrey Crowther, then editor of The Economist, "If the economic relationships between nations are not, by one means or another, brought fairly close to balance, then there is no set of financial arrangements that can rescue the world from the impoverishing results of chaos."[30]

These ideas were informed by events prior to the Great Depression when — in the opinion of Keynes and others — international lending, primarily by the U.S., exceeded the capacity of sound investment and so got diverted into non-productive and speculative uses, which in turn invited default and a sudden stop to the process of lending.[31]

Influenced by Keynes, economics texts in the immediate post-war period put a significant emphasis on balance in trade. For example, the second edition of the popular introductory textbook, An Outline of Money,[32] devoted the last three of its ten chapters to questions of foreign exchange management and in particular the 'problem of balance'. However, in more recent years, since the end of the Bretton Woods system in 1971, with the increasing influence of Monetarist schools of thought in the 1980s, and particularly in the face of large sustained trade imbalances, these concerns — and particularly concerns about the destabilising effects of large trade surpluses — have largely disappeared from mainstream economics discourse[33] and Keynes' insights have slipped from view.[34] They are receiving some attention again in the wake of the Financial crisis of 2007–2010.[35]

Physical balance of trade

Monetary balance of trade is different from physical balance of trade[36] (which is expressed in amount of raw materials, known also as Total Material Consumption). Developed countries usually import a lot of primary raw materials from developing countries at low prices. Often, these materials are then converted into finished products, and a significant amount of value is added. Although for instance the EU (as well as many other developed countries) has a balanced monetary balance of trade, its physical trade balance (especially with developing countries) is negative, meaning that a lot less material is exported than imported. For this reason, activist talk about the issue of ecological debt which implies a sort of predatory economic system. The nature of the trade balance statistics is such that is conceals distorted material flow.

United States trade deficit

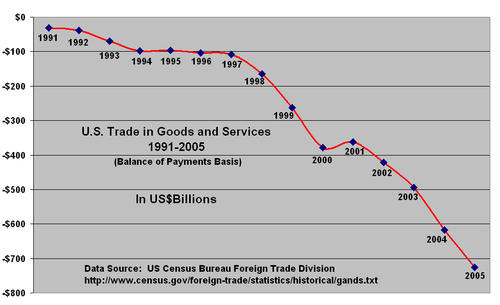

The U.S. has held a trade deficit starting late in the 1960s. It was this very deficit that forced the United States in 1971 off the gold standard. Its trade deficit has been increasing at a large rate since 1997 [37] (See chart) and increased by 49.8 billion dollars between 2005 and 2006, setting a record high of 817.3 billion dollars, up from 767.5 billion dollars the previous year.[38]

The graph indicates that, as Frédéric Bastiat predicted, the deficit slackened during recessions and grew during periods of expansion. Also of note, many economists calculate trade deficits and/or current account deficits as a percentage of GDP. The US last had a trade surplus in 1975.[39] Every year there has been a major reduction in economic growth, it is followed by a reduction in the US trade deficit.[26]

See also

- List of the largest trading partners of the United States

- Current account

- Balance of payments

- FRED (Federal Reserve Economic Data)

- List of countries by current account balance

- Marshall–Lerner condition

Notes

- ↑ Sullivan, Arthur; Steven M. Sheffrin (2003). Economics: Principles in action. Upper Saddle River, New Jersey 07458: Pearson Prentice Hall. pp. 462. ISBN 0-13-063085-3. http://www.pearsonschool.com/index.cfm?locator=PSZ3R9&PMDbSiteId=2781&PMDbSolutionId=6724&PMDbCategoryId=&PMDbProgramId=12881&level=4.

- ↑ Now attributed to Sir Thomas Smith; quoted in Fernand Braudel, The Wheels of Commerce, vol. II of Civilization and Capitalism 15th-18th Century, 1979:204.

- ↑ 3.0 3.1 3.2 3.3 Bivens, L. Josh (December 14, 2004). Debt and the dollar Economic Policy Institute. Retrieved on July 8, 2007.

- ↑ MAJOR FOREIGN HOLDERS OF TREASURY SECURITIES. U.S. Treasury.gov

- ↑ Roberts, Paul Craig (August 7, 2003). Jobless in the USA Newsmax. Retrieved on May 6, 2007.

- ↑ 6.0 6.1 Hira, Ron and Anil Hira with forward by Lou Dobbs, (May 2005). Outsourcing America: What's Behind Our National Crisis and How We Can Reclaim American Jobs. (AMACOM) American Management Association. Citing Paul Craig Roberts, Paul Samuelson, and Lou Dobbs, pp. 36-38.

- ↑ See Roberts, Loc. cit.

- ↑ Paul Craig Roberts (07/28/04)."Global Labor Arbitrage".VDARE. Retrieved on July 7, 2009.

- ↑ Whitney, Mike (June 2006).Labor arbitrage. Entrepreneur. Retrieved on July 7, 2009.

- ↑ The shift away form thrift.The Economist, April 7 2005.

- ↑ Free Trade Bulletin no. 27: Are Trade Deficits a Drag on U.S. Economic Growth? | Cato's Center for Trade Policy Studies

- ↑ Causes and Consequences of the Trade Deficit: An Overview

- ↑ Bivens, Josh (September 25, 2006 ).China Manipulates Its Currency—A Response is Needed. Economic Policy Institute. Retrieved on February 2, 2010.

- ↑ David Friedman, New America Foundation (2002-06-15).No Light at the End of the Tunnel Los Angeles Times.

- ↑ Sir Keith Joseph, Centre for Policy Studies (1976-04-05).Stockton Lecture, Monetarism Is Not Enough, with forward by Margaret Thatcher. (Barry Rose Pub.) Margaret Thatcher Foundation (2006).

- ↑ 16.0 16.1 Phillips, Kevin (2007). Bad Money: Reckless Finance, Failed Politics, and the Global Crisis of American Capitalism. Penguin. ISBN 9780143143284.

- ↑ 17.0 17.1 Cauchon, Dennis and John Waggoner (October 3, 2004).The Looming National Benefit Crisis USA Today

- ↑ George W. Bush (2006) State of the Union. Retrieved on April 17, 2009.

- ↑ Bailey, David and Soyoung Kim (June 26, 2009).GE's Immelt says U.S. economy needs industrial renewal.UK Guardian.. Retrieved on June 28, 2009.

- ↑ Smith, Adam. (1776). An Inquiry into the Nature and Causes of the Wealth of Nations, Indianapolis: Liberty Fund, 1981, 2 vols., (1776) (reprint of the Clarendon Press edition, Oxford 1976, with Edward Cannan's original index from 1922)

- ↑ Price Theory, Chapter 6: Simple Trade

- ↑ Free to Choose video series from PBS

- ↑ Hume, David (1987). "Essays, Moral, Political, and Literary". Liberty Fund, Inc. http://www.econlib.org/library/LFBooks/Hume/hmMPL28.html.

- ↑ ""David Hume: The Concise Encyclopedia of Economics"". 2008. http://www.econlib.org/library/Enc/bios/Hume.html. Retrieved 2009-03-20.

- ↑ Dougherty, Carter (October 19, 2007). "Dollar Hits a New Low, Oil Hits a New High". The New York Times. http://www.nytimes.com/2007/10/19/business/worldbusiness/19euro.html?ref=worldbusiness. Retrieved April 26, 2010.

- ↑ 26.0 26.1 Michael M. Phillips, World Economy in Flux As America Downshifts

- ↑ Bastiat: Selected Essays, [1]

- ↑ http://www.berkshirehathaway.com/letters/growing.pdf

- ↑ Crowther, Geoffrey (1948). An Outline of Money. Thomas Nelson and Sons. p. 326–9.

- ↑ Crowther, Geoffrey (1948). An Outline of Money. Thomas Nelson and Sons. p. 336.

- ↑ Crowther, Geoffrey (1948). An Outline of Money. Thomas Nelson and Sons. p. 368–72.

- ↑ Crowther, Geoffrey (1948). An Outline of Money. Thomas Nelson and Sons.

- ↑ See for example, Krugman, P and Wells, R (2006). "Economics", Worth Publishers

- ↑ although see Duncan, R (2005). "The Dollar Crisis: Causes, Consequences, Cures", Wiley

- ↑ See for example,""Clearing Up This Mess"". 2008-11-18. http://www.monbiot.com/archives/2008/11/18/clearing-up-this-mess/. Retrieved 2009-01-09.

- ↑ Physical Trade Balance, OECD Glossary of Statistical Terms

- ↑ http://www.census.gov/foreign-trade/statistics/historical/gands.txt

- ↑ FTD - Statistics - Country Data - U.S. Trade Balance with World (Seasonally Adjusted)

- ↑ http://usinfo.org/enus/economy/trade/docs/06s1288.xls

External links

- Are Trade Deficits a Drag on U.S. Economic Growth?

- Graph of Historical U.S. Net Export of Goods and Services

- Where Do U.S. Dollars Go When the United States Runs a Trade Deficit? from Dollars & Sense magazine

- The Economic Impact of a U.S. Slowdown on the Americas from the Center for Economic and Policy Research

- OECD Trade balance statistics

- U.S. Government Export Assistance

|

||||||||||||||||||||